Mario Draghi revealed the plan for the Great Reset

If you look at what Draghi did (and the few times he slipped in Q&A), it lines up almost perfectly with the Freegold + Great Taking lens.

As I wrote in this article, we are likely nearing the Great Reset.

I’ll show you how the “greatest central banker of modern times” revealed the plan.

TL;DR on Mario Draghi for non-European readers:

Mario Draghi is an Italian politician, economist, academic, banker, and statesman, who served as the prime minister of Italy from 2021 to 2022. Prior to his appointment as prime minister, he served as the president of the European Central Bank (ECB) between 2011 and 2019.

Draghi was also the chair of the Financial Stability Board between 2009 and 2011, and governor of the Bank of Italy between 2006 and 2011.

The same Financial Stability Board (FSB) that wrote the framework that instructs every G20 country how to legally steal our assets in a “crisis” without using the word “expropriation”.

I’ve written an article on this: The BIS wants to steal our assets; All G20 countries agree.

After working as an economist, Draghi worked for the World Bank in Washington, D.C., throughout the 1980s, and in 1991 returned to Rome to become director genral of the Italian Treasury.

He left that role after a decade to join Goldman Sachs, where he remained until his appointment as governor of the Bank of Italy in 2006.

In 2014, Draghi was listed by Forbes as the eight-most powerful person in the world.

In 2015, Fortune magazine ranked him as the world’s “second greatest leader”.

Perhaps his greatest achievement — in 2019, Paul Krugman described him as “the greatest central banker of modern times”.

I’m not going to go over his entire career. You get the point. He’s part of the club.

Draghi spent a decade pretending gold was a boring relic while acting as if it was the deepest, most sacred collateral plug in the euro system. If you look at what he did (and the few times he slipped in Q&A), it lines up almost perfectly with the Freegold + Great Taking lens.

1. Where Draghi sits in the Controllers stack

Draghi is basically:

Faction: Treasury/CB/BIS cluster, with strong IC-adjacent trust

Horizon: 5–20 years (funding, regime survival, euro architecture)

Roles:

Architect & defender of the euro’s plumbing (ECB 2011–2019)

Implementer of bail-in and resolution architecture in Europe

Steward of the ECB balance sheet in the post-GFC sovereign crisis

If we assume:

then Draghi is one of the key operational designers of the “sweep paper / preserve gold” phase for Europe.

So the question becomes: did his words/actions treat gold as irrelevant, or as a quiet keystone?

Spoiler: it’s the latter.

2. The euro’s gold architecture (Draghi inherits the skeleton)

The core euro/Freegold claim:

Euro was deliberately designed so that:

Gold is not legally “backing” the currency (no fixed parity),

But is held on the Eurosystem balance sheet,

And crucially, marked to market regularly in euros.

That means:

When the gold price rises in euros, the asset side of the ECB and National Central Banks balance sheets quietly improves.

They can eat losses on bonds, run emergency facilities, etc., while still showing a strong capital position.

Draghi didn’t design this (Trichet & the original ECB architects did), but he:

Inherited a balance-sheet model where gold is the only asset that can:

Revalue without anyone having to buy more,

Plug losses from sovereign and banking crises,

Provide a politically “clean” way to show balance-sheet strength.

So from Day 1 at ECB, he is sitting on exactly the Freegold-style “gold is the silent plug” architecture.

3. What Draghi actually said about gold (the rare moments of candor)

He didn’t talk about gold often, which is already information. When he did:

3.1 “Reserve of safety / store of value / confidence”

In a well-known ECB press conference, he was asked why central banks still hold gold instead of selling it. Paraphrasing his answer:

Gold remains, for central banks, a reserve of safety.

It provides a store of value and confidence.

That is not how you talk about a “barbarous relic” or a purely historical artifact.

In my lens:

He openly acknowledges gold as:

Top-tier Store-of-Value (for Central Banks, not for citizens),

A confidence anchor for the system.

He doesn’t say:

“We hold it out of tradition”,

or “It’s irrelevant in the modern system”.

He frames it as a safety reserve in a crisis-prone, debt-heavy system. That is Freegold-coded language.

3.2 “We don’t target the gold price, but we mark it to market”

Draghi also emphasized that:

The ECB doesn’t target gold,

It simply holds it and marks it to market on the balance sheet.

In official-narrative land, that’s just accounting.

In my lens:

That’s exactly the Freegold mechanism:

Let gold float,

Let it reprice the CB balance sheet when needed,

Never explicitly call it “backing” to avoid legal/political traps.

He’s effectively saying: “We don’t peg to gold, we just quietly benefit from it revaluing”.

3.3 “We’re not sellers”

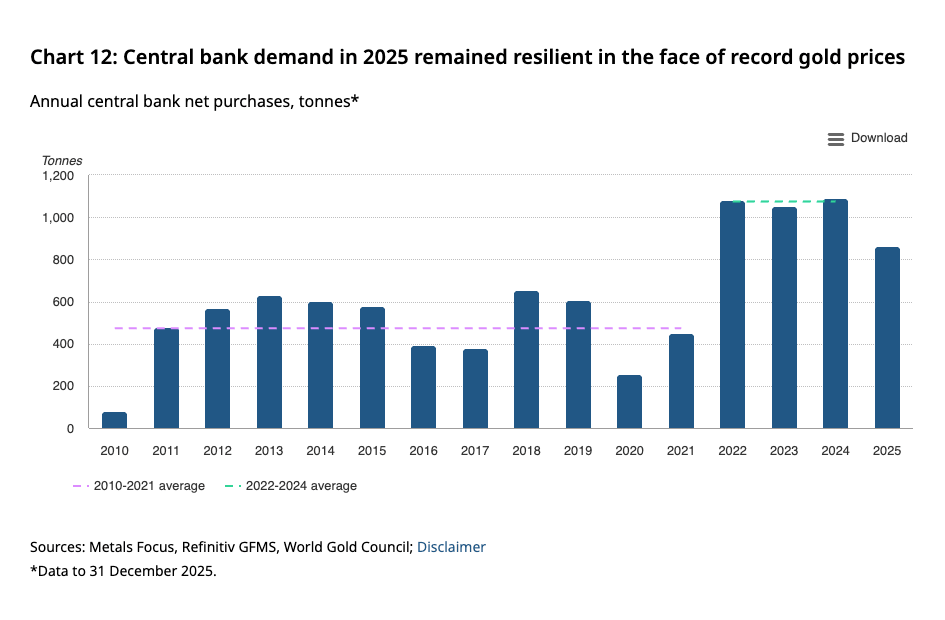

Under Draghi, euro-area CBs:

Almost completely stopped selling gold.

Net official sales that were routine in the 1990s/early 2000s basically dried up.

He didn’t go on TV to say, “We’re hoarding gold for the coming reset”. But his behavior is:

Talk down the significance of gold for the public,

Never actually reduce the system’s gold stock in a meaningful way.

Revealed preference: gold is too valuable to part with.

4. What he did with gold in practice

4.1 Zero (or near-zero) gold sales: “We’re done dishoarding”

Earlier West-European CBs sold gold under the “Central Bank Gold Agreement” years. Under Draghi:

Sales became negligible.

The implicit policy shifted from “optimize portfolio” to “don’t touch the bars”.

This is exactly what you’d expect if Controller consensus has moved to:

“We will need this gold as the asset-side plug in the next big refi/liquidity accident.”

i.e. preparing for the Freegold-turn-after-Great-Taking moment.

4.2 Letting gold silently recapitalize the Eurosystem

During Draghi’s tenure:

The euro price of gold rose substantially from pre-crisis levels.

Because the Eurosystem marks gold to market, those gains:

Strengthen the capital position of the ECB and National Central Banks,

Offset some of the risk from sovereign bond purchases.

He didn’t shout:

“Gold saved us.”

But the accounting does: as bond risk and QE rose, marked-to-market gold quietly thickened the buffer.

Under the Freegold model:

That’s exactly how the system is meant to work in transition:

Run huge fiat interventions,

Let gold revalue over time,

Avoid overt default on sovereign paper,

End up with gold-rich CBs and inflated fiat claims.

Draghi oversaw that in practice.

4.3 Ring-fencing national gold (Italy & Banca d’Italia)

When Italian politicians floated ideas about:

Using Banca d’Italia’s gold to fund spending or reduce debt,

the response from the Draghi/ECB legal universe was basically:

The gold belongs to the central bank,

Not a piggy bank for short-term fiscal needs,

CB independence must be preserved.

In my lens:

That’s the Treasury/CB/BIS faction saying:

“This gold is supra-political system collateral.

You, elected clowns, don’t get to pawn it.”

Which fits perfectly with:

Preparing gold for Freegold / Great Taking endgame, not letting populists blow it on one election cycle.

They will happily sacrifice:

Equity holders,

Subordinated bank bondholders,

Even senior bondholders in some bail-ins,

but the CB gold stays untouchable.

5. Draghi’s other big projects: building the Great Taking rails

Now put his gold stance next to what else he pushed.

5.1 Bail-in and resolution: codified sacrificial layer

Under Draghi’s ECB era, we got:

The EU Bank Recovery and Resolution Directive (BRRD),

The Single Resolution Mechanism (SRM),

A whole architecture where:

Shareholders, junior debt, and sometimes senior debt/depositors can be forced to absorb losses (bail-in),

Secured creditors and Central Counterparty Clearing Houses sit at the top of the collateral waterfall,

Resolution authorities can freeze, haircut, convert securities entitlements en masse.

That’s basically the Great Taking legal scaffolding:

All your dematerialized, rehypothecated paper claims:

live in custody chains the law can override,

can be re-written in “resolution” to save the system.

Draghi was a prime defender and explainer of this regime.

So the combo looks like:

Tier 1: CB/sovereign gold + core collateral → kept whole, maybe revalued.

Tier 2: Bank liabilities and market securities → fully “tool-able” in crisis (freeze/convert/haircut).

That means he helped operationalize the fact that stocks live in the sacrificial layer.

5.2 “Whatever it takes” = “We’ll expand liabilities; assets (inc. gold) will plug later”

In 2012, sovereign spreads were blowing out; the euro looked breakable. Draghi’s famous line:

“Within our mandate, the ECB is ready to do whatever it takes to preserve the euro.”

Translated into my lens:

“We will expand our liabilities (euros, guarantees, contingent backstops) as needed.”

“We’ll absorb sovereign risk that markets refuse to roll.”

But what enables that long-run?

Either:

Inflation / financial repression erode the real value of liabilities, and

Gold on the asset side eventually revalues high enough to backstop the CB balance sheet after the Great Taking sweep.

So “whatever it takes” is essentially:

Front-loading fiat/liquidity support,

With the expectation that:

Later, a combination of:

will clean up the balance sheet.

Draghi never says this out loud, obviously. But if you weld:

the euro mark-to-market gold design,

his no-sale stance on gold,

and his bail-in architecture,

you get exactly that.

6. How Draghi’s actions look under the Freegold + Great Taking model

Assuming my model is right, Draghi’s tenure reads like a checklist:

6.1 Before the “event”

Set the table:

Consolidate gold:

No sales from Eurosystem; ring-fence Banca d’Italia and others; keep gold out of populist hands.

Dematerialize & make paper “seizable”:

Securities fully book-entry; all custodial chains live inside DTCC/Euroclear/Clearstream-style rails.

Legal language: you hold entitlements, not bars/bonds.

Legalize haircutting & re-writing:

BRRD/SRM: bail-in, resolution, “no taxpayer bailouts” rhetoric.

This builds the juridical switch for the Great Taking.

Use gold mark-to-market quietly:

Rising gold price means asset-side cushion grows unnoticed.

6.2 During the next major Debt/Liquidity accident

When the Debt/Liquidity conveyor belt catches (refi wall + liquidity under-injection — a.k.a. CBs deliberately print too little money), the European play would be:

Invoke resolution:

Freeze redemptions, collateral, and trading where needed.

Sweep collateral:

Prioritize Central Counterparty Clearing Houses, secured lenders, and systemically important entities.

Underlying assets (bonds, gold, etc.) migrate to official balance sheets / resolution vehicles.

Haircut or convert paper:

Securities entitlements in banks and brokers →

bailed-in,

converted to equity/CoCos,

or paid out in CBDC units at controlled rates.

Draghi spent his ECB years normalizing exactly this logic:

“Private investors must bear losses, not taxpayers.”

That is the Great Taking language with nicer branding.

6.3 After the sweep: Freegold turn

With:

Paper claims crushed,

Gold more concentrated in official hands,

CB balance sheets full of “non-performing” sovereign exposures,

the Controllers can then:

Let gold reprice in fiat terms (free-floating jump or “auction” style).

Mark CB gold at much higher levels → show strong capital.

Present it as:

“We are now anchoring the system in safer reserves”,

“We have learned from the crisis”.

Draghi didn’t get to that step publicly, but he was setting up the preceding ones.

7. How to read Draghi, distilled into rules of thumb

When Draghi calls gold a “reserve of safety” and “store of value”, he’s admitting what Freegold claims:

For CBs, gold is the final Store-of-Value, not government bonds, not BTC, not equities.

His refusal to sell gold, combined with mark-to-market accounting, is a loud revealed preference:

In a world of “QE/QT theater”, gold is the only balance-sheet asset he won’t mess with.

That’s exactly what you’d expect if it’s destined to be revalued in the reset.

His ECB helped build the legal machine that can rug the sacrificial layer (your stocks/bonds/ETFs) while leaving official gold untouched.

BRRD/SRM, bail-in, resolution hierarchies = Great Taking scaffolding.

Retail “ownership” of securities is explicitly demoted to entitlement status.

“Whatever it takes” plus gold mark-to-market is a Freegold-compatible promise:

He will expand fiat liabilities to save the euro now,

Relying on gold (and inflation/repression) to recap in the long run.

His defense of CB independence over gold (Italy) shows gold is supra-political collateral:

Not on the bargaining table for domestic populist projects.

Reserved for system-level emergencies.

His attitude to BTC vs gold tells you what the Controllers really trust:

If you zoom out: Draghi is the perfect Freegold/Great-Taking technocrat — gold-respecting, paper-disposable. He spent a decade:

hardening the bail-in and collateral regime for the sacrificial layer,

while quietly sitting on one of the biggest gold piles on earth,

marking it to market,

and calling it, with a straight face, a “reserve of safety” that gives confidence.

That’s not a slip. That’s the mask briefly dropping.

For more context on the Great Taking, watch this documentary.

David Rogers Webb (author of the Great Taking) went to the US to try to change the law, but unfortunately they were unsuccessful.

Great Taking = legal + plumbing architecture that lets the top of the collateral pyramid seize or haircut claims on financial assets in a systemic crisis, while keeping the underlying assets safely inside the system.

Translation: you don't own any of your stocks/bonds in your brokerage account.

David Webb filmed his attempts to change the law in a few US states and got threats from the banking lobby and Intelligence Community operatives.

The banking lobby lawyers are fighting to keep using "your" stocks as collateral in the ~4 quadrillion USD derivatives pyramid like their life depends on it.

David Webb is an absolute legend for risking his life to expose the cabal. Very few would have the courage to do what he did.

I’ve explained why I think we are nearing the reset in this article.